Last week, the Central Bank of Ireland published an important consultation paper. Despite the boring title (“Macro-prudential policy for residential mortgage lending”) this is a very important initiative that will have profound implications for banking and the Irish property market.

The paper proposes the introduction of restrictions on Loan-to-Income (LTI) and Loan-to-Value (LTV) ratios for Irish residential mortgages. Specifically, it proposes that a maximum of 20 percent of loans should have LTIs over 3.5 and that a maximum of 15 percent of loans should have LTVs in excess of 80 percent. The latter, in particular, would represent a significant departure from the lending standards seen in Ireland over the past few decades.

Given the recent experience in Ireland and elsewhere with property bubbles, I agree that measures of this type need to considered as part of the regulatory policy kit. So, as a general matter, the Central Bank are to be congratulated for being willing to introduce this type of regulation despite its inevitable unpopularity in certain quarters.

In particular, I support the proposed LTI restrictions. These restrictions may be unpopular now with first-time buyers. For example, someone with an income of €50,000 will now be told that the most they can borrow is €175,000. This may appear to reduce their ability to purchase a house if, for example, they had previously planned to borrow €250,000. However, evidence from previous cycles has shown that more generous mortgage credit tends to drive up house prices. This has meant that first-time-buyers end up chasing their own tails, as they all take on additional debt without actually being able to buy better houses. I would be confident that, over time, the LTI limits will restrain house prices and allow first-time buyers to obtain a home without being burdened with huge debts.

That said, I still have some concerns about the way these measures are being introduced and about their timing. In particular, I have reservations about the rapid introduction of an 80 percent LTV standard.

Consultation and Debate

After the global financial crisis, it has become widely accepted that macroeconomic policy-makers need to look beyond using only short-term interest rates to control the economy. Restrictions on LTV and LTI ratios are examples of a set of policy options that have become known as “macro-prudential policy” i.e. policies that are aimed at protecting the stability of the financial system as a whole rather than just focusing on each financial institution separately.

Central Banks, as financial regulators, will generally be the organisations imposing macro-prudential policies. This has caused some debate about the implications of independent central banks setting a much wider range of policies than in the past. Here, for example, are some thoughts from the IMF’s chief economist, Olivier Blanchard.

If you think now of central banks as having a much larger set of responsibilities and a much larger set of tools, then the issue of central bank independence becomes much more difficult. Do you actually want to give the central bank the independence to choose loan-to-value ratios without any supervision from the political process. Isn’t this going to lead to a democratic deficit in a way in which the central bank becomes too powerful? I’m sure there are ways out. Perhaps there could be independence with respect to some dimensions of monetary policy – the traditional ones — and some supervision for the rest or some interaction with a political process.

I don’t claim to have all the answers as to how these new tools should interact with the political process. Still, I do think the Central Bank’s approach appears to be at odds with Blanchard’s ideas. The approach being taken to debate and consultation has been pretty minimalist.

These policies will have a direct effect on the housing decisions of many people and will probably also have important indirect effects. As such, I believe the measures should have been subjected to a longer and more rigorous consultation process, involving a series of public meetings and Oireachtas committees prior to the specific proposals being tabled. As it is, the Bank is announcing a very short consultation process with the plan being to take comments up to December 8 and then introduce very substantial changes to mortgage lending in January.

Cyclical Considerations

One of the themes of academic work on macro-prudential policies is that these policies should be used in a cyclical fashion, tightening credit during upturns and allowing it to be loosened during downturns. My reading of the recent international evidence on the use of LTV caps is that they are being used in countries where the authorities are very concerned about the risk of a housing crash, with the implicit policy being to ease these restrictions when this risk is lower.

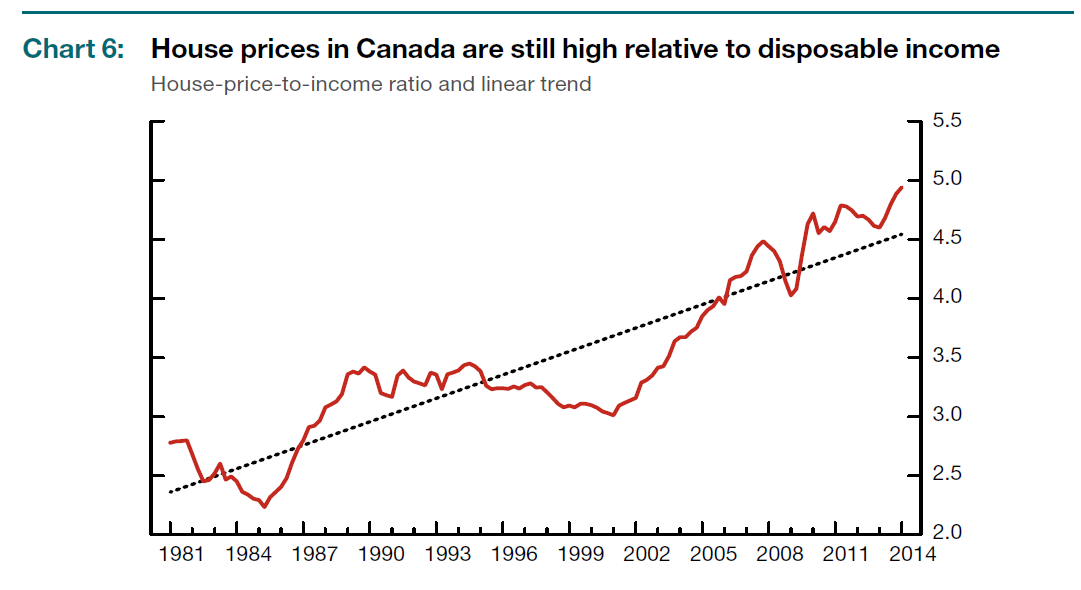

For example, Canada is a widely-cited example of a country where a set of restrictions on LTVs have been introduced, with maximum LTVs gradually being reduced from 100 percent in 2008 to 80 percent in 2012 (along with various other measures – see this summary from the IMF). However, it is worth emphasising that these measures have been put in place because the Canadian authorities view a large housing crash as a significant possibility. Here is a chart from the latest Bank of Canada Financial System Review showing a steady rise in housing valuations.

The commentary in the report views a housing crash as a potentially severe threat to Canadian banks and the restrictions on lending are being put in place for this reason.

New Zealand is another example of a country that has introduced LTV restrictions, with loans with LTVs above 80 percent now restricted to be no more than 10 percent of the total amount of mortgage lending. Here is a nice paper from the Reserve Bank of New Zealand describing the restrictions. An important message from this paper, however, is that the RBNZ views these restrictions as an explicitly temporary policy.

LVR restrictions are to be used only occasionally, at those points in the financial cycle where there is a real danger of growing systemic risks leading to financial instability. The Reserve Bank does not intend to operate LVR restrictions in a continuous fashion to smooth the cycle, but rather aims to limit the extreme peaks in house price and housing credit cycles.

This raises questions about the current situation in the Irish housing market. Is Ireland now in a situation where, in the absence of these policies, there would be a significant risk of a crash over the next few years?

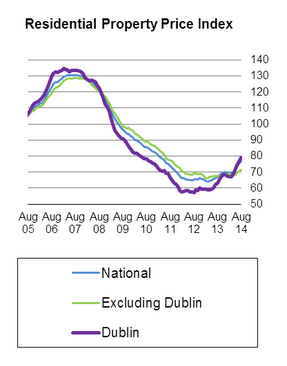

Residential property prices are certainly growing a very fast pace, up 15 percent in the year ending in August. But, as the picture below shows, prices are still very far off peak levels.

More broadly, valuations look to be in line with the more sustainable levels seen prior to the housing boom. For example, the ratio of prices to rents is back at levels last seen in the late 1990s.

The Central Bank’s new policies are focused on restricting the downside of house price declines by restricting the provision of mortgage credit. However, the current trend of rising prices is not in any way related to easy mortgage lending. Indeed, the Central Bank’s own statistics show that the total stock of mortgage credit continues to decline at about the same pace as it has over the past three years (see the red line below).

Rather than being driven by credit, the evidence points to a shortage of supply as the main factor driving house prices. After the building binge of the Celtic Tiger years, housing completions have slumped. Indeed, given trends in population and household formation, we now appear to be at the point where the previous period of over-building has now been offset by the cumulative under-building of recent years.

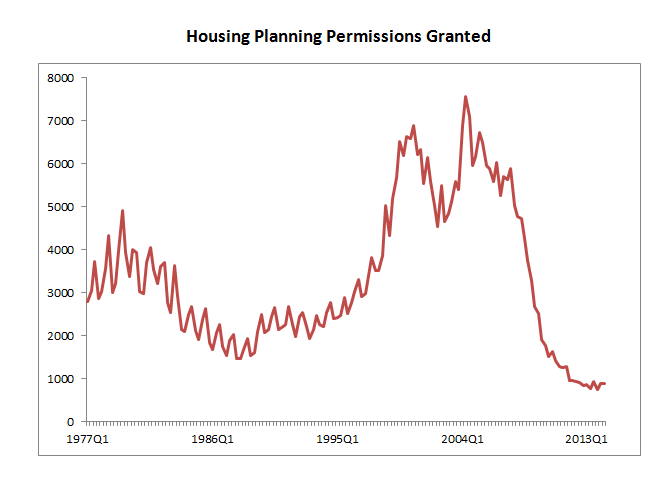

Nor does it appear that recent price increases are doing much yet to provoke a supply response. Planning permissions remain at historically low levels. Anecdotal evidence suggests restrictions on the supply of credit to builders as well as a raft of cost-increasing building regulations are at least partly responsible for this lack of supply response.

Against this background, there are reasons to be concerned about the potential impact on the housing sector of the proposed 80 percent LTV requirement in January. As of now, most first-time buyers have been focused on saving about 10 percent of the value of the home. Particularly for those who are also currently paying rent, coming up with this 10 percent is already a challenge. An instant doubling of this requirement would likely force a large number of potential purchasers out of the market, as they would need to wait another few years to double their savings.

This measure may well end up stabilising house prices but it may reflect the deliberate engineering of a nasty equilibrium, one in which Central Bank regulations lead to low demand for new house purchases, matched on the other side by a low level of supply due to credit and other regulatory restrictions. Meanwhile many potential buyers (particularly those unable to sufficiently tap the Bank of Mum and Dad) will feel squeezed out of home ownership and forced to rely on Ireland’s chaotic rental market or its already-inadequate supply of social housing.

At this point, my assessment is that conditions in the Irish housing market do not currently point towards the need for a sudden large change in LTV limits. Whether a gradual introduction of higher LTVs is desirable is a more open question.

LTV versus LTI Restrictions

I noted above that the situations in which countries like Canada and New Zealand have introduced LTV restrictions look quite different from the situation in Ireland today. Indeed, it seems highly unlikely that the authorities in Canada or New Zealand would be imposing 80 percent LTV caps if their property market looked like the current Irish market.

In addition, it is worth noting that LTV restrictions are not a necessary part of the macro-prudential toolkit. The UK has also begun adopting macro-prudential policies aimed at cooling a property market that (in places anyway) shows signs of being genuinely over-heated. However, the Bank of England’s new guidelines have focused solely on LTI restrictions rather than limits on LTVs.

Even in expansions, LTV limits can have unfortunate knock-on effects. Here’s a nice article from the Telegraph on macro-prudential policies. It contains the following observations from Adair Turner.

“The trouble with LTV is it can be a bit circular. You impose an LTV limit and the price can go up, and then somebody can borrow more money via a mortgage on the price that’s gone up,” he says. “One of the problems we have in our economy is the way in which we borrow money against the value of an asset which goes up, which appears to make more borrowing justified. LTI targets the real thing, which is: can people repay the debt out of their income?”

In this sense, a policy framework that focuses too much on LTV restrictions can enhance the fundamental pro-cyclicality that is already in place with existing banking regulations.

Needed: An Integrated Housing Policy

The benefits to financial stability of requiring a large deposit before purchasing a house are clear. Banks are less likely to lose money on home loans in a downturn once the owners have put in more equity. However, the risk associated with falling house prices in Ireland are relatively low at this point and the sudden imposition of an 80 percent LTV norm will have implications for society that go well beyond banks.

It’s not rocket-science to point out that anything that makes it harder for people to purchase something (an inward shift in the demand curve in economist jargon) will result in a lower amount of purchases of that item. The imposition of significantly higher LTVs will likely delay the age at which younger people can purchase homes and will increase the amount of people who will never be in a position to purchase a home.

But housing is special in the sense that we all need a roof over our head, so any policy that reduces people’s ability to purchase homes needs to be matched with a policy that helps them with alternatives such as social housing or long-term renting. Ireland is currently doing a horrible job in this area. The boom provided an opportunity to build up a good stock of high quality social housing but governments decided they had other priorities. Renters also have relatively weak rights, meaning those who want long-term security feel they must own their own home.

These are all issues that the government can act on over the next few years. So I have no problem with Ireland setting a long-term target of an 80 percent LTV norm in the context of a sensible integrated housing policy. But I believe the conditions for the macro-prudential use of LTV restrictions do not apply to the current Irish housing market and that LTI restrictions make better macro-prudential policy tools anyway. As such, I fear the unintended consequences of the LTV policy may outweigh its perceived longer-term benefits.

The concluding lines of the Reserve Bank of New Zealand paper by Lamorna Rogers (cited above) are relevant to the current debate in Ireland.

LVR restrictions provide a way of restraining housing demand while working on the supply response. But in the medium to longer term, imbalances will need to be resolved through appropriate longer run policy measures, including actions to improve the housing supply.

It is, of course, crucially important that Ireland does not return to the irresponsible mortgage lending of the last decade. However, what is required now is more than that: Ireland needs a coherent joined-up housing policy. Ideally, it would be better to debate restrictions on LTVs as part of this broader discussion instead of imposing them for financial stability reasons irrespective of the other parts of the policy framework.