After Mario Draghi’s hints that the ECB is getting ready to purchase large quantities of Spanish and Italian bonds, expect to read lots of commentary claiming “the ECB is taking huge risks with its balance sheet”, that “the ECB risks becoming insolvent, endangering the future of the euro” or that “Eurozone states may have to recapitalize the ECB at huge cost to taxpayers”.

Much of this commentary is based on misunderstanding the facts about the Eurosystem’s balance sheet and the meaning of central bank balance sheets. In this post, I want to briefly explain what a central bank balance sheet is, then go through the basic facts about the capital position of the Eurosystem of central banks and then argue that the common focus on central bank solvency is misplaced.

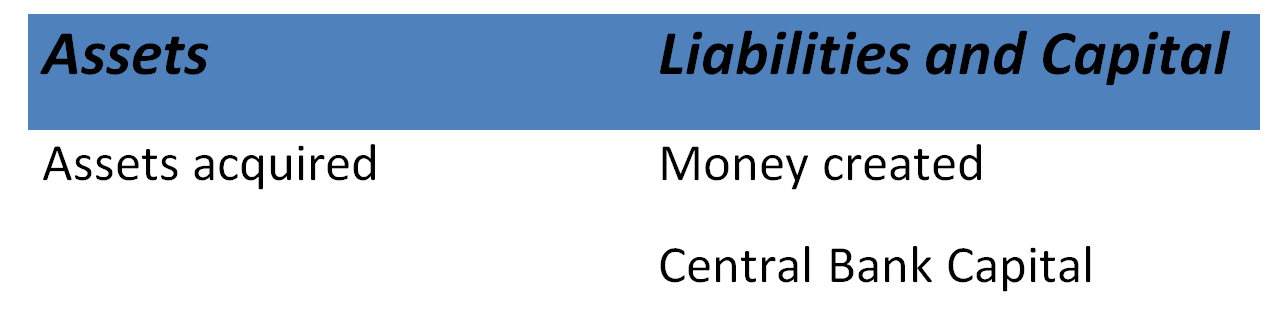

Central Bank Balance Sheets

Like all businesses, central banks publish balance sheets that show their assets and liabilities. However, central banks are not just any business. They have the power to print money that is accepted as legal tender. So their assets have been acquired via printing of money. Central banks list the money they have created as liabilities and the gap between the current value of their assets and liabilities is labelled “capital”.

So a stylized central bank balance sheet looks as follows.

If a central bank purchases assets that then decline in value, it could end up having negative capital. When a commercial bank has negative capital, it is termed insolvent and either re-capitalised or shut down. The “insolvent” terminology is sometimes applied to a central bank in this situation but, as I discuss below, central banks are unique organizations and this phrase isn’t particularly appropriate.

Bond-Buying Risk: Eurosystem not ECB

A common confusion that arises when people discuss potential losses stemming from sovereign bond purchases or loans to banks comes from the assumption that the risk of these operations lies with the European Central Bank. For example, it is common to see commentary that examines the ECB’s balance sheet and concludes that the ECB faces a significant risk of becoming insolvent. This is because the ECB lists “Capital and Reserves” of only €6.5 billion, a tiny amount relative to the likely scale of bond purchases likely to be executed under the Securities Market Programme (SMP).

In fact, the ECB also has revaluation accounts and provisions, both of which can cover losses, worth €30 billion. More importantly, the risks associated with the bond-buying program are in fact shared across the ECB and all of the national central banks in the Eurosystem. So what matters when thinking about the threat to solvency of the SMP is the size of the Eurosystem’s capital resources.

The ECB releases a Eurosystem financial statement every week. Currently, it shows capital and reserves of €86 billion and revaluation reserves of €409 billion. These figures show the Eurosystem would have to incur much larger losses on its bond purchases than is often believed before the question of insolvency would become an issue.

Would Eurosystem Insolvency Matter?

This still raises an interesting question. What would happen if the ECB published its weekly balance sheet one day and it showed negative capital? For many commentators, the answer is apocalyptic. The euro will have lost all credibility as currency, hyper-inflation will ensue, that kind of thing.

In truth, the answer is that not much at all would happen. The euro is a fiat currency. In other words, unlike the days of the gold standard, the Eurosystem does not promise to swap the euro at some specified rate for another asset such as gold. The currency is not “backed” by the central bank’s assets.

Since central bank money costs next to nothing to create, the “Liabilities” on its balance sheet are essentially notional. Indeed, a central bank’s asset holdings could fall below the value of the money it has issued – the balance sheet could show it to be “insolvent” – without impacting on the value of the currency in circulation. A fiat currency’s value, its real purchasing power, is determined by how much money has been supplied and the various factors influencing money demand, not by the stock of central bank assets.

Taken to an extreme, one could argue that a central bank with sufficiently negative capital could face problems implementing monetary policy because its stock of assets may be so low as to limit its ability to sell assets to reduce the supply of privately circulating money. However, detailed analytical research by ECB economists Ulrich Bindseil, Andres Manzanares and Benedict Weller concludes that

central bank capital still does not seem to matter for monetary policy implementation, in essence because negative levels of capital do not represent any threat to the central bank being able to pay for whatever costs it has. Although losses may easily accumulate over a long period of time and lead to a huge negative capital, no reason emerges why this could affect the central bank’s ability to control interest rates.

Despite the absence of reasons to be concerned about negative central bank capital, it is still unlikely that such an outcome would be allowed to continue in the Eurozone. The actual rules relating to central bank solvency seem a bit murky but it is generally understood that any element of the Eurosystem that had negative capital would need to be recapitalized by governments providing them with assets.

Even then, these “recapitalizing” transactions wouldn’t actually have any effect on the net asset position of Eurozone governments because central banks hand over their profits to the government. For example, suppose a government hands its central bank a bond that pays €500 million in interest each year. That raises the net income of the central bank by €500 million and thus raises the amount that is handed back to the government by €500 million. The bond has no net cost to the government.

By these comments, I’m not suggesting that bond purchase programs have no cost. To the extent that they involve increasing the money supply, they can contribute to inflation so there is an implicit cost for all citizens. But this is the reason central banks need to be careful with their purchases; concerns about central bank solvency are beside the point.

Unfortunately, despite its lack of substantive importance, the idea that the Eurosystem needs to be protected from balance sheet insolvency has featured heavily in discussions of policy options. Indeed, it is well known that senior ECB officials are extremely concerned with protecting their balance sheet and have employed their “risk control framework” to protect themselves from losses at many of the key moments in the euro crisis.

One can only hope that the policy debate about the upcoming bond purchases focuses on things that matter, like the future of the euro, and not on things that don’t, like the ECB’s capital levels.