A few weeks ago, I was a discussant for a very interesting paper by Patrick Honohan reviewing Ireland’s banking crisis. My comments are here.

Category Archives: Irish Economy

#ItsNotUCDItsTheGovernment

The students union at my university are staging a protest tomorrow against the university’s management. It being Valentine’s day, the campaign features a broken heart and a slogan #ItsNotMeItsUCD. Other tweets in the campaign complain about how UCD has become a “commercialised university”, use the hashtag #NotaBusiness and contain dark murmerings about “corporate interests”. The campaign wants action from UCD management on a number of issues.

I fully understand student unhappiness with campus rents being high, with campus services not being better and various other ways in which UCD has sought to either raise income or reduce costs. I have no role in the management of the university and I don’t wish to defend the management for every decision they have taken but … I think this campaign completely misses the actual source of these problems which is the massive reduction in government funding provided to Irish universities.

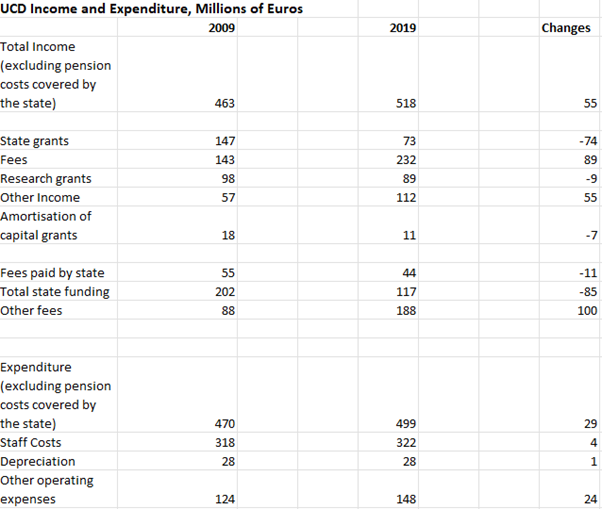

The table below shows comparable estimates of income and expenditure by UCD comparing 2019 with 2009 (the last accounts published are for 2020 but that was a strange year for the university’s finances so I’ve used 2019 instead). The figures come from here.

A few items are worth highlighting.

- UCD is not a profit-making business. It has no shareholders or “corporate interests” to pay dividends to. The money the university earns gets spent on paying for staff and services and keeping the university operating. In other tables in the financial reports you can see that there is no large endowment of money to pay for things. The university generally keeps enough cash on hand to run the university for a few months but no more than that.

- Total state funding for UCD from fees and grants fell by €85 million between 2009 and 2019, even as the economy recovered and government coffers flowed over. The state took away about 20% of the cost of funding UCD during the recession and did not return this funding when the economy improved.

- Despite this, UCD increased spending over this period with most of the additional spending going on “other operating expenses”. Spending on student facilities increased from €3 million in 2009 to €4.8 million in 2019.

- The additional spending was possible because the university increased fees from other sources by €100 million and because they raised an additional €55 million from other sources. The largest part of the increase in fee income came from Irish undergraduates having to pay a €3000 fee (a policy introduced by the government to cover much of the cost of reduced state funding) but the university also raised a lot of additional fees from non-EU students. €19 million of the increase in other income came from rents from student residences.

The bottom line in terms of what happened to Irish universities over the last decade is that the Irish government effectively walked away from funding them properly and told the universities to go raise their own income to pay for the provision of third level education.

The SU want UCD to earn less income from rents and fees and to spend more on student services and staff salaries. I’d love all of that to happen but the reality is that, as things stand, this would open a huge gap between UCD’s income and expenditure and the funding to allow that is not there. The only way there can be a large increase in spending and a corresponding reduction in income is if UCD were to get back some of the state funding that was taken away.

There is a long tradition of student unions protesting against their own university and, in many cases, they pick good causes and help to improve the world. In this case, I’m afraid UCD SU have picked the right cause but the wrong target. Ironically, this protest comes at a time when there appears to be some debates within the Cabinet about providing better funding for the university sector. Those in government who don’t want to provide more money for universities or to cut fees will be relieved that tomorrow’s protest is focused at UCD’s management rather than the Department of Higher Education or the Department of Public Expenditure.

The reality is that in the absence of a serious change in state funding, there will be no improvements in the areas the SU cares about. And blaming UCD management won’t help them come up with a magic money tree that allows more spending with lower income.

Brexit: One Clarification and One Concession the EU Could Offer the UK

After a chaotic two months in British politics and with little time remaining before the UK is set to leave the EU, its parliament has now requested the EU replace the crucial backstop protocol in the Brexit withdrawal agreement with some other set of unspecified “alternative arrangements.” The Prime Minister reversing course on the deal she agreed after two years of intensive negotiations was never likely to go down well with the EU27 and the immediate negative response from Donald Tusk suggests there will be no re-opening of negotiations.

Simply ignoring this latest request may work out for the EU. After a few more weeks without progress, enough MPs may finally decide that the impending chaos of no deal is worse than the deal Theresa May agreed to in November and which is still on the table. The UK could end up signing up to the November agreement, though this would be seen as a humiliating outcome for many of the politicians who enthusiastically voted for last night’s “Brady amendment”.

There are a number of reasons, however, why the EU, and particularly Ireland, should be wary of pursuing this strategy and I suggest they should consider an alternative route involving a clarification and a concession on the backstop.

The reasons to be wary?

First, without further negotiations or concessions, it is possible that the UK parliament may end up delivering a no-deal outcome that very few profess to want. In the absence of a deal that can pass the House of Commons, even after a potential delay of the Article 50 process, the no-deal crash out becomes the default option and odds on it continue to rise. The Brady vote has probably entrenched some Conservative MPs into a position they will find difficult to give up without some movement from the EU. It may make no economic sense whatsoever for the UK to exit without a deal but Brexit has never made economic sense and its most intense advocates are growing ever more determined to leave at almost any cost. The EU member state that would be most damaged by this outcome would be Ireland.

Second, the strategy of providing no response at all to the Brady vote could poison EU\UK relations and their North\South equivalent in Ireland for many years even if the November agreement is eventually passed. Many in the UK will feel, rightly or wrongly, that they were bullied into the agreement by the EU without appropriate considerations for the perceived problems associated with the backstop. In Northern Ireland, the DUP will claim the backstop was imposed by the EU against the preferences of a majority of the House of Commons. Unionist objections about a lack of democratic legitimacy of the backstop, in which Northern Ireland remains subject to EU regulations and customs rules but has no say in deciding those rules, will continue to be a cause of discontent for many years.

So what could the EU do to respond to last night’s vote?

A Clarification

Firstly, the EU could clarify that it has no objections to the UK leaving the joint customs union with the EU after the transition period, provided Northern Ireland remains within the EU’s customs union and aligned on goods regulations.

Brexit wonks could argue that this clarification shouldn’t really be necessary since this is the original version of the backstop that the EU offered, so it should be clear they are willing to still offer this. The all-UK backstop was a hard-won concession to the UK. It reduced the amount of trade disruption to be experienced over the medium-term by the UK while it was still negotiating trade deals with the EU and the rest of the world, and it prevented the need for customs checks on goods going from Great Britain to Northern Ireland.

Still, the nature of the all-UK version of the backstop does not seem to have been well understood in Westminster, partly because Theresa May never spent any time explaining its benefits. Instead, among Brexiters, it has become widely held that this all-UK backstop is an attempt to “trap” the UK permanently within EU structures and hamper it from successfully negotiating its own trade deals.

A simple clarification from the EU on this issue, to be added to the political declaration, could help to resolve this unnecessary confusion about the all-UK backstop.

A Concession

That still leaves the question of the Northern Ireland element of the backstop. Theresa May probably did not devote much political capital to selling the fact that Great Britain could move out of the backstop without difficulty provided Northern Ireland remained in it because she was determined to keep the DUP on board and they would not have been pleased with this being sold as a positive feature. As it is, in addition to losing many Tory colleagues who disliked the all-UK backstop, May also failed to get the DUP to support her November agreement and has now acceded to their request that she ask the EU to modify the backstop.

So what can be done? The motivations of the EU and Irish government for the backstop proposal are well known and there are severe limits on how much they can move. Moreover, the nebulous mooted “alternative arrangements” to the backstop mentioned in the Brady amendment don’t present a useful basis for current discussions.

However, the EU could do the following: Use the political declaration to offer the citizens of Northern Ireland a referendum on whether to remain within the EU’s customs union and single market five years after the beginning of the operation of a Northern-Ireland-only backstop. This referendum could be repeated at perhaps ten-year intervals thereafter. Should a referendum show the people of Northern Ireland wanted to exit the backstop, the EU would agree jointly with the UK to end this arrangement.

I have proposed the idea of a referendum within Northern Ireland before, back in November 2017. I still think an approach of that sort should have been considered and polling suggests the backstop would have received majority support. It is too late now to consider a referendum of this sort prior to the UK exiting the EU. However, a promise to hold a referendum five years after the end of the transition period would provide a clear concession to those who believe the backstop arrangements would be harmful to Northern Ireland by offering them a chance to convince their fellow citizens to end the arrangements after a period.

This proposal would also give the citizens of Northern Ireland a number of years to experience “life in the backstop” and to consider the benefits and costs associated with it before making their own decision about whether to continue with this arrangement. I have detailed previously how the backstop would probably provide some important benefits for the Northern Ireland economy and that the perceived intra-UK frictions associated with it are likely to cause only minor difficulties compared with the far larger problems associated with a hard intra-Irish border. The costs and benefits of being excluded from future UK trade deals may also become more apparent. I suspect it may turn out that Northern Ireland consumers and farmers won’t actually be too concerned about missing out on the chlorinated chicken and hormone-injected beef brought about by trade deals with the United States or South American countries.

The Irish government and EU could also offer to work to address concerns about the “democratic deficit” associated with the backstop. It may be possible for Northern Ireland to have non-voting members of the European Parliament or for the Irish delegation of MEPs to include a couple of delegates elected via votes from those in Northern Ireland. The EU could regularly hold workshops and listening tours in relation to upcoming regulatory changes that could affect Northern Ireland as long as it remains in the backstop.

Another benefit of this proposal is that it would allow at least seven years for the UK and Irish governments to explore more fully the options for “smart border” technologies which have been widely promoted by some and heavily doubted by others. A well-funded joint project by the EU and UK on the possibilities available could be prepared to provide concrete information to Northern Ireland’s voters on the way the border would operate should they ever choose to leave the backstop. My guess is that no matter how smart the technologies, a hard border of some sort would be required if the backstop is removed but this proposal would give Ireland and the EU at least seven years to prepare for this potential outcome.

The danger of this approach from the perspective of the Irish government is that it may only kick the can of a hard border down the road by seven years or more. But it may also help to avert a no-deal Brexit and provide invaluable time to prepare Irish firms for potential future arrangements. One could also argue that if the backstop arrangements cannot receive majority support in Northern Ireland over time, then they are probably not politically sustainable anyway.

Would This Be Enough to Get the Deal Through the UK Parliament?

Would these clarifications and concessions be enough to avert a hard Brexit? It’s hard to know but a final attempt at outreach could at least convince some MPs that the EU and Ireland have listened and addressed their concerns about the UK’s ability to conduct future trade deals and the democratic legitimacy of the backstop for Northern Ireland.

I suspect the DUP will not accept a proposal of the sort outlined here but these ideas may be enough to convince sufficient numbers of Tory waverers and Labour leavers that the deal on the table represents a better outcome than no deal. In addition to helping pass the withdrawal agreement, a final effort of this sort from Ireland and the EU could hopefully also set a tone for a more co-operative future relationship with the UK.

The EU’s Backstop is a Great Opportunity for Northern Ireland

The past week has been the most fraught yet in the Brexit negotiations. The EU and UK have not agreed on how the “Irish backstop” proposed in December should operate. The UK government and the DUP are unhappy that the EU believes the “backstop” arrangement should only apply to Northern Ireland. The EU backstop would essentially keep Northern Ireland (but explicitly not the rest of the UK) in the EU customs union and single market unless other arrangements are agreed that would also rule out the need for a hard Irish border.

In Westminster and Northern Ireland, there is a lot of concern about the EU’s proposal, with many viewing it as implying a “border in the Irish sea” and Theresa May arguing that it would “threaten the constitutional integrity of the UK” and that “no UK prime minster could ever agree to it”. In Northern Ireland, unionists have argued this approach is inconsistent with UK’s commitment in the December agreement that there would be “unfettered access for Northern Ireland’s businesses to the whole of the United Kingdom internal market”. Arlene Foster has repeatedly insisted that this arrangement would be “catastrophic” for the Northern Ireland economy and, in a notable upping of the ante, said on Friday that the EU’s approach would amount to Northern Ireland being “annexed” from the UK.

I believe these concerns are fundamentally misplaced. Rather than being threatened economically, Northern Ireland would gain from the implementation of the EU’s backstop. To understand why, let’s look at how the backstop would work in practice.

Unfettered Access

Let’s start with the most obvious objection to the EU’s backstop: the idea that a “sea border” would make it harder for Northern Irish firms to sell into Great Britain. The DUP’s Arlene Foster has emphasised this repeatedly in recent months. Consider, for example, this statement from Foster in March

“What was there, in the [EU draft agreement] legal text, is around creating a border down the Irish Sea,” she said.

“And of course that’s not something we in Northern Ireland could allow from a constitutional point of view, but also in terms of economics, it would be catastrophic to have a border down the Irish Sea.”

“56% of our goods from Northern Ireland go to Great Britain, so it is incredibly important that that border does not exist.

This probably sounds like a reasonable concern but it is without foundation. Firms in Northern Ireland will remain within the UK, so there will not be and cannot legally be customs checks for goods produced in Northern Ireland when travelling to the rest of the UK. In addition, the UK itself promised in the December agreement that unfettered access would be maintained for Northern Irish firms and that “no new regulatory barriers” would affect these firms. Together, these points mean Northern Irish firms will have unfettered access to the rest of the UK under the EU backstop.

If you’re surprised by this and perhaps think I’m making it up, you might not know the UK civil service has already worked out how this backstop would work and they have said there would be unfettered access for Northern Ireland firms for the rest of the UK market. The document describing how this would work was part of a series of UK civil service documents leaked to politicians in the European Parliament and was discussed in various press stories in May.

This “customs channel” proposal implies no land border checks on the island of Ireland but some checks at the small number of ports in Northern Ireland that transport goods to Great Britain. Goods would either go through a “green channel” with no checks or a “red channel” which has checks. Crucially, goods from firms in Northern Ireland would go through the green channel. Goods coming from the Republic of Ireland to the Great Britain via Northern Ireland’s ports would probably have to go through the red channel if the UK required customs or regulatory checks on goods from the EU.

Viewed this way, the “border in the Irish sea” terminology is misleading because it will not affect firms from Northern Ireland. A better terminology would be “enforcing the land border at Northern Ireland’s ports.” With a small number of ports in Northern Ireland, all of whom are already checking shipping documentation of some sort, the implications for trade frictions for Irish firms would be far less severe than the alternative of enforcing customs and regulatory checks on a meandering 310 mile border with about 200 different crossing points.

Over time, various issues would need to be sorted out about how this arrangement would evolve. These issues are not trivial but they would be would not be too difficult to work out between the EU and UK. A few examples.

- Most likely, Northern Ireland would be given a “special economic zone” status, so that the free movement of goods from its firms to both the rest of the UK and EU is agreed and accepted internationally by all members of the WTO.

- Assurances may be required that the UK will discourage tariff-hopping via “name plate” firms setting up in Northern Ireland just to label products as a way to avoid tariffs that the UK may charge on EU goods (though these tariffs should be minimal if the EU and UK agree a sensible free trade deal).

- Some goods moving from Great Britain to Northern Ireland may need to be checked to make sure they meet EU regulatory requirements. Goods that are heading on towards the Republic of Ireland would also need to have EU customs procedures applied.

- The UK has promised there would be no new regulatory barriers affecting Northern Irish firms accessing the market in Great Britain. If the UK starts passing new product regulations that deviate from the EU’s, any new regulatory bill passing parliament could include a clause stating that Northern Ireland’s products (produced according to EU rules) are also allowed to be sold throughout the UK, i.e. that there is a form of regulatory equivalence. Ultimately, it is up to the UK government to honour its promise to allow Northern Irish firms unfettered access to markets in Great Britain and there should be little difficulty in implementing this.

Economic Impact on Northern Ireland

So the EU backstop isn’t going to turn Northern Ireland into an economic dystopia. It is far more likely to have a positive economic effect. Northern Ireland would become the only place where firms could export freely to both the EU and the UK. One could easily imagine Northern Ireland obtaining new foreign direct investment because of this unique selling point. Business leaders in other regions of the UK (for example Scotland) would view this kind of special status as a great opportunity if they could attain it but the EU has made clear that this can only apply to Northern Ireland.

Northern Ireland’s agriculture and food sector is also likely to do better under this regime than under any alternative approach. If the UK decides to pursue trade deals that allow cheap food from outside the EU into the UK, then Northern Irish farmers would have to compete with these imports in the Great Britain market (most likely in an environment with less generous state-funded agricultural subsidies). However, regulatory alignment with the EU would mean produce like chlorinated chicken and hormone-injected beef could not be sold in Northern Ireland, providing some protection for local producers. Northern Irish farmers would still also have full access to the European Union market without facing tariffs or quotas, which would provide some opportunity to diversify their sales.

Most importantly, the EU’s backstop keeps the land border open and allows the all-island Irish economy to continue to operate freely. Contrary to Boris Johnson’s uninformed sneering, the reality is that more firms in Northern Ireland sell goods to the Republic than to Great Britain and integrated all-Ireland supply chains are of huge importance to many firms, North and South. Northern Ireland would keep this important element of its economy, without losing anything.

Constitutional Integrity? Annexation?

But what about the constitutional integrity of the United Kingdom which is supposedly a great concern to Theresa May? Well the UK’s constitutional integrity is a complicated thing, not least because it doesn’t actually have a constitution.

The reality is the UK has a patchwork of different governance arrangement across its regions. Northern Ireland, in particular, already differs sharply from the rest of the UK in lots of ways, including its form of government, rules on gay marriage and abortion and the plethora of ways in which the Good Friday agreement has introduced North-South co-operation. In truth, the DUP’s desire for Northern Ireland to have a different corporate tax rate from the rest of the UK is probably a more substantive difference in economic policy than anything new that would emerge from the proposed backstop.

Is this Northern Ireland getting annexed by the EU or Republic? Clearly not. Northern Ireland would still send MPs to Westminster. Its people would still pay UK tax, hold British passports (if they wish), have access to the NHS and the UK social welfare system, and be subject to UK laws in most areas. The people of Northern Ireland would probably barely notice their new status. By contrast, they would certainly notice the return of a hard border, which is the most likely alternative option if the EU’s backstop offer is rejected.

The Politics: Still Time (Just About) for a Broader Discussion

It now looks like nothing will be settled between the UK and EU until the Autumn. This still leaves some time for an informed debate in Northern Ireland and Westminster about the consequences of the EU backstop proposal. For a number of reasons, this debate has not taken place so far and there is a general lack of understanding about how the EU backstop would work. These reasons include:

- Northern Ireland does not have an assembly operating. The assembly would certainly have held extensive committee meetings to discuss the various options and this would have helped to debunk the scaremongering about the so-called “border in the sea”.

- Many in the UK government probably know the EU backstop would work well for Northern Ireland. Under other circumstances, they could give assurances to everyone in region that the backstop would work well for them – it is not the EU’s job to explain how unfettered access to the UK market could be maintained. However, the Conservatives are reliant on a hard-line unionist party for their majority at Westminster and do not want to upset the party keeping them in power by asking them to consider a proposal they are so uncomfortable with.

- The last UK general election meant the DUP and Sinn Fein were the only parties in Nothern Ireland with MPs and Sinn Fein do not attend parliament. This has left the Westminster debate without nationalist or non-sectarian voices (such as the Alliance Party) who could have argued for the EU’s backstop. It is also seems likely that the current DUP leadership has handled these issues in a more aggressive manner than, for example, Peter Robinson would have (see for example Robinson’s speech last week imploring leaders on both sides of the community to compromise to get the Assembly up and running again.)

- Finally, the Irish government appears to have outsourced most of the communication on Brexit to Michel Barnier (who has a lot on his hands) rather than working hard to publicly explain the benefits of the EU backstop to all sides of Northern Ireland’s community.

Northern Ireland may not have a functioning assembly but the MLAs that were elected last year must surely understand they have a political responsibility for what happens next. Even if the assembly does not formally convene again this year, it must be possible for the MLAs to meet to debate the options and perhaps hold a “consultative vote” on the EU backstop. The DUP do not speak for all of Northern Ireland (they received 29% of the vote in the 2017 assembly elections) and they should not be the only party with an influence on the final outcome. Even if it had little legal standing, a vote by a majority of assembly members registering approval for a form of the EU backstop would have a profound political impact.

A final word on the long-term political implications. The DUP clearly believe that Northern Ireland remaining in the EU’s customs union and single market is a step towards a united Ireland. I doubt if this outcome would actually change perceptions of a united Ireland by much since it would mainly involve a continuation of the status quo for most people in Northern Ireland. Indeed, a special economic zone status within the UK but with full access to the EU could be popular even with some nationalists. However, the alternative outcome – the return of a hard land border with Northern Ireland firms having poorer access to the EU – may convince many nationalists that they are better off to re-join the EU via unification. With a border poll sufficient to trigger unification, a rejection of the backstop may turn out to be a crucial stop on the road towards (rather than away from) a united Ireland.

Brexit and the Irish Border: Let Northern Ireland Decide?

Seventeen months on from the Brexit vote, the UK government has largely avoided setting out clear and realistic positions on key issues. Their stance on almost everything continues be a form of cake-and-eat-it.

Nowhere is this more clear than on the question of the Irish border. The UK’s position is that there will be no hard Irish border even though they plan to take the UK out of the EU’s single market and customs union. When pressed on this, they use the phrases “flexible and imaginative” and “technologies” but don’t put forward much by way of specifics. (If you think I’m exaggerating, read this).

In the absence of anything concrete from the UK government, the EU has put forward its own flexible and imaginative suggestion that Northern Ireland could remain part of the EU’s single market and customs union. This proposal has been received negatively by the Conservative Party and the DUP. As best I can tell, there has been little public discussion of the objections that have been put forward, so here I want to discuss the economic arguments for and against the EU’s proposal and to propose that Northern Ireland be allowed vote on it.

The Economic Arguments

If Northern Ireland were to remain part of the EU’s single market and customs union, then this would allow free movement of goods between the North and South of Ireland. However, once the UK leaves the EU’s single market and customs union, then there would need to be some form of checks on goods leaving Northern Ireland for Great Britain as well as those goods coming in the other direction. The extent of these checks would depend, over time, on the extent to which the UK departs from its current EU-consistent policies on tariffs and regulations.

One economic argument against this proposal is that Great Britain is a more important market for Northern Irish firms than the Republic of Ireland and the rest of the EU. Figures show that in 2015, Northern Ireland had €14.4 billion in final sales to Great Britain while final sales to Ireland were €2.9 billion and sales to the rest of Europe were €2.1 billion. In this sense, surely it makes sense from an economic perspective for Northern Ireland to rule out any trade barriers with Great Britain?

There are two counter-arguments to this position. The first is that the final sales figures under-state the significance of cross-border economic linkages to Northern Ireland. The second is that the inconvenience to firms of NI\GB trade costs will likely be much smaller than the costs associated with an Irish border for goods.

Importance of the All-Ireland Economy

The trade figures just described come from an appendix to the UK government’s position paper on Northern Ireland and Brexit. However, the paper also acknowledges that

the sale of finished products to Great Britain relies upon cross-border trade in raw materials and components within integrated supply chains meaning trade with both Great Britain and Ireland are vital to Northern Ireland’s economy.

And that cross-border trade is a crucial part of the Northern Irish economy:

Over 5,000 businesses in Northern Ireland exported goods to Ireland in 2015, one and a half times as many as sold goods to Great Britain.

So cross-border trade clearly plays a very significant role in Northern Ireland’s economy. In addition to these substantial linkages, there are also a wide range of all-Ireland bodies devoted to supporting all-Ireland economic linkages in areas such as agriculture, the environment, energy and so on. Northern Ireland leaving the EU’s single market would likely undermine the economic benefits that have been achieved in these areas.

A Seamless Irish Border?

Once the UK leaves the EU’s customs area and agrees new trade deals with third-party countries, then the EU will require an Irish customs border to protect the integrity of its customs union. There is no point, by the way, in presenting this as a “big undemocratic EU bullies little Ireland” story: There is no way Irish farmers will allow the UK to pursue cheap food deals with the US or Brazil and then have these products imported to the Republic without customs checks.

Brexiteers are currently saying the EU will be “to blame” for the subsequent border checks but the border will only be there because of the UK’s decision to leave the EU. Moreover, despite silly talk from various British politicians about the UK “not being bothered” to enforce a customs border in Ireland, the UK will be under legal obligations to do so via its WTO commitments.

So if Northern Ireland leaves the single market, the customs union and European Economic Association (EEA), there will be border-related checks on goods: Customs checks, rules-of-origin checks, regulatory compliance checks. Will the much-discussed technological solutions make all of this seamless? No

Some in the British press have pointed to the Sweden-Norway border as an example of how well an Irish border could work. For example, this BBC report starts with stories about average wait times of eight minutes and plans for a future frictionless border. Only later in the story do we find “there is still plenty of paper to be processed, first with the customs agents, then at the customs office” and that the eight-minute figure might have been over-hyped. “A Swedish trucker grumbles to me that it can take an hour and a half, and he is unimpressed with the level of customer service.”

For lots of reasons, an Irish customs border will be more complicated. For starters, unlike Norway, the UK will be leaving the EEA, meaning extra layers of trade and regulatory checks will be required that do not exist on the Norway-Sweden border. Another important difference is the political sensitivities of border checks in Northern Ireland and the possibility that formal checkpoints could be a target for terrorist organisations.

The complexities of the physical Irish border are also daunting. Currently, there are an estimated 1.85 million cars crossing the border each month through about 200 crossing points as well as 208,000 light vans and 177,000 lorries. And the nature of the border they are crossing? Here’s Fintan O’Toole

It meanders for 310 miles, and it is not a natural boundary. It was never planned as a logical dividing line, still less as the outer edge of a vast twenty-seven-state union. It is simply composed of the squiggly boundaries of the six Irish counties that had, or could be adjusted to contain, Protestant majorities in 1921. And it cannot be securely policed. We know this because during the Troubles it was heavily militarized, studded with giant army watchtowers, overseen by helicopters, and saturated with troops—and it still proved to be highly porous. It is an impossible frontier.

Trade Costs Associated with an Irish Border

Even if physical customs borders managed to be relatively seamless, Northern Ireland leaving the customs union would still damage many of the businesses that rely on integrated cross-border supply systems. To give one example, consider the example of dairy businesses in which milk from Northern Ireland is moved over the border for processing, then perhaps moved back to the North for further processing and then perhaps sold in the Republic. When Michael Lux, a German customs expert and former European Commission employee was asked about these kinds of businesses by a House of Commons committee, he responded

“I am always saying to companies, “You need at least two people doing the customs business, if you do it yourself, because one of them may be ill or on holiday and then you will have nobody to do it.” Alternatively, you can use a service provider that is a logistics company. Depending on the complexity, they will charge you between €20 and €80 per declaration; so the cost will increase enormously just due to the fact that, each time you are doing something that involves a crossing of the border, it creates a cost. That will be part of the cost of the milk and, later, of the cheese, and I cannot imagine that anybody will continue these practices. It would just be too costly.”

Manufacturers in Northern Ireland are gradually learning how costly it would be for them to leave the customs union. Stephen Kelly, Chief Executive of Manufacturing Northern Ireland, told a Commons committee:

I have some evidence here for the Committee today, on just what that country-of-origin certification and the paperwork around that would actually mean in terms of cost to an individual business. Between the development and the time required to produce those certificates, plus the letters of credit from banks that are required to export alongside, the total is £478 per shipment. That is roughly the same price as shipping a container from Northern Ireland to GB or two-thirds of the price of shipping a full container from south-east Asia to Northern Ireland ….

the dangers that are staring our members directly in the face right now is a £478 charge every time they transfer anything across a border, and that is just the paperwork element of it, never mind any tariff elements

To summarise, even a sophisticated “light touch” implementation of an Irish customs border would involve delays and costs that would have a highly negative effect on businesses that have relied on integrated North-South supply chains.

Trade Costs Associated with Northern Ireland Remaining in the Customs Union

What about the alternative? Wouldn’t trade costs associated with Northern Irish firms moving goods to Great Britain also be a big problem? This is clearly not an ideal scenario but there are a number of mitigating points.

The first is that this is a much simpler “border” to monitor. Almost all of Northern Ireland’s trade with Great Britain is shipped via freight and two-thirds of this is shipped via Belfast port (see page 10 here). Goods are shipped already require various pieces of paperwork to be filled out, so it may be possible to add customs and regulatory forms to these and, yes, to use technology to ensure that all of the trucks arriving at Belfast port are ready to board with minimal delays. It would certainly be a lot easier than monitoring the famously-complicated Irish border.

A second is that it may be possible for the EU and UK to agree to designate Northern Ireland as a special economic zone that would allow streamlined procedures to make moving goods to Great Britain as cheap as possible. This could include exemptions from various regulatory or rule-of-origin checks for the vast majority of Northern Irish firms and a guarantee from the UK government that there would be no fees charged for any documentation required. I would guess the Irish government would be willing to share in the costs of administering the checks required in moving goods from Northern Ireland to Great Britain.

This outcome—remaining in the customs union and single market but with simple low-cost procedures for moving goods into the UK—could make Northern Ireland a highly attractive option for international firms. It would allow them to get direct access to EU markets while also getting lower-cost access to the British market. Designed in a flexible and imaginative way, Northern Ireland could potentially prosper as a result of its special status.

Movement of People

One complication when discussing Brexit is that when borders get discussed, most people immediately think about passport control and delays in travel for people moving through airports. Thus, the idea of Northern Ireland remaining in the EU customs union gets represented as a “border in the Irish sea” and people imagine that Northern Irish residents will have to go through passport control to get into Great Britain. In fact, Northern Ireland remaining part of the customs union and single market would likely have no implications for border controls for people. It would simply affect the movement of goods.

Both the Irish and British government seem committed to maintaining the “common travel area” which would allow Irish and British people to move freely between the two countries as well as maintaining other rights such as the right to work. I don’t believe anyone is suggesting Irish border controls to monitor people coming from the EU going to Belfast to then enter the UK.

Indeed, the whole focus on border controls as a way of keeping EU citizens out of the UK is misplaced. Unless the UK is planning to eliminate tourism from the EU, there will presumably be a bilateral agreement between the UK and EU on a light-touch visa-free system allowing tourist visits of sixty to ninety days. The UK will have to decide how to deal with those who overstay these visas but absent the right to work legally in the UK, I doubt if this is going to be a major problem. And there would really be little point in coming to Ireland to travel to Belfast to enter the UK with plans of working illegally since you could just go directly.

So let’s leave aside issues relating to passport controls: If Northern Ireland remains in the EU customs union and single market, its people will be able to move freely back and forth to “the mainland”.

The Politics

So that’s the economics of it. Neither of the options on the table are ideal and none will match the current level of market access enjoyed by firms in either the North or South of Ireland. But, on balance, a plan to keep Northern Ireland as part of the EU’s single market and customs union probably has more economic benefits for Northern Ireland than costs.

The politics are infinitely more complicated. The largest party in Northern Ireland, the Democratic Unionist Party (DUP) define themselves by their commitment to maintaining Northern Ireland as part of the UK and they resist anything that looks like it is loosening these links. Hence, the reaction of DUP’s leader to the EU’s proposal as “reckless” and all about the Irish government “getting the best deal for themselves”. Similarly, the Conservative Party seem dumbfounded at this idea, with the Secretary of State for Northern Ireland, James Brokenshire commenting “I find it difficult to imagine how Northern Ireland could somehow remain in while the rest of the country leaves. I find it impossible.”

DUP opposition to the EU proposal has also not been helped by implications that the proposal is part of an Irish plan to somehow fast-track reunification. I think this is misplaced. The current Varadkar\Coveney Irish leadership team strikes me as perhaps the least republican in Irish history. And one can believe this is the best proposal available without being in any way focused on a united Ireland. Personally, I would vote against a united Ireland if it was put to a referendum in the Republic and would worry greatly about the economic, political and security capacity of the Republic to successfully absorb Northern Ireland.

So even if worries about “a border in the Irish sea” (which sounds like every unionist’s nightmare) could be clarified and the economic costs of a hard Irish border explained, it is likely that most DUP supporters will accept the economic costs of the new Irish border rather than accept anything that looks like a step towards integration with the Republic. And to be fair, unionists may wonder what their status as UK residents actually means if they started to depart from the regulatory framework of a post-Brexit UK (e.g. if Northern Ireland didn’t get to be part of the Brexiteer vision of the UK as the Singapore of Europe).

The reality, however, is that Northern Ireland already differs sharply from the UK in lots of ways, including its form of government, rules on gay marriage and abortion and the plethora of ways in which the Good Friday agreement has introduced North-South co-operation. The proposal to stay in the customs union could be considered just an additional recognition that Northern Ireland is a very specific place with a special status and its impact may likely be far less obvious than the re-introduction of border controls on the island.

Also, DUP opposition to the EU proposal is not, on its own, reason to assume it should not be considered. The DUP only received 28 percent of the vote in the recent Assembly elections, with the anti-Brexit Ulster Unionist Party receiving 12 percent and the anti-Brexit anti-hard-border Nationalist parties receiving 40 percent. Indeed, many young people in Northern Ireland are moving past the simplistic Nationalist\Unionist identities and may consider voting for whichever option they believe will be good for their economic security.

A Proposal: Let Northern Ireland Decide

Northern Ireland voted against Brexit by a fairly comfortable 56 to 44 margin but that was a vote for all of the UK to remain in the EU. We don’t know how Northern Ireland would vote on a proposal to remain in the EU’s customs union and single market while the rest of the UK does not. But I believe the people of the North deserve the opportunity to make this decision.

A future Northern Ireland economic model dictated by either London or Brussels could prove to be a long-standing source of resentment to large numbers of people in the North. In contrast, a future economic model decided by a referendum would continue the approach of requiring democratic consent for major decisions that was established with the Good Friday agreement.

So my recommendation to the Irish government is as follows: Agree to allow the Brexit talks to move to Phase 2 in return for a commitment from the UK to hold referendum in Northern Ireland by May 2018 on the EU’s proposal for it to remain part of the single market and customs union.

This proposal gives both the UK and Irish government a way out of what currently seems to be an impasse: Ireland can claim to have found a route to maintain the all-Ireland economy, while the UK government can get on with what it really cares about (trade talks) without actually taking the decision to keep Northern Ireland in the single market and customs union.

Is it feasible for the UK government to implement this proposal given its parliamentary reliance on the DUP? I think so. The DUP will doubtless object to a referendum but a British parliamentary majority for the proposal should be easy to obtain with the support of the Labour Party. After they’ve decided whether to bring the UK government down (thereby losing all the money Theresa May promised them and potentially letting Jeremy Corbyn take over) the DUP can then campaign again to get Northern Ireland out of the single market and customs union. If people of Northern Ireland decided to agree with them, then everyone in Ireland would need to prepare for the border that would be the consequence.

Flat Tax Calculations for Ireland

Flat tax systems, featuring a single rate and the elimination of tax breaks, have a lot to be said for them. They allow for the reduction of marginal tax rates and thus increase incentives for employment and discourage tax avoidance. And despite misconceptions related to the “flat tax” terminology, these systems can be made as progressive as you like via the introduction of a tax credit or tax-exempt allowance. In addition, many of the tax breaks that are eliminated are designed to benefit the wealthy. I’ve written about this before, highlighting that it is possible to combine a flax tax system with progressivity.

Given the potential benefits of a flat tax system, I’m glad that RENUA, one of Ireland’s new political parties, has proposed a such a system (see here and here) as it may lead to a constructive debate about what we want from our income tax system.

As with most economic policy proposals, however, the devil is in the details, and an examination of the evidence suggests some of RENUA’s claims about its flat tax proposal are over-egged and that the headline rate proposed would radically increase inequality.

Supply-Side Over-Egging

RENUA are proposing a 23% flat tax rate, supplemented by a basic income policy in which people are guaranteed an income of €8000. The first problem with the proposal is that it is likely to raise far less revenue than the current system. RENUA’s statement discusses this as follows

Our conservative projections across the income bracket show that this rate of tax will generate approximately 75%-80% of the existing income tax head of taxation. As people will retain 77% of their current income and of any additional income they earn on top of this, secondary factors and multiplier effects will generate more than the remaining 20% of the current rate of collection.

Anyone who follows fiscal policy debates in the US will probably be aware that this kind of “dynamic scoring” of tax proposals is a famously thorny issue (a “can of worms” according to Harvard’s Greg Mankiw). However, in examining this literature (see this presentation for example) it is clear that a 20% boost to revenue collection is well above the usual range of estimates for what can be expected from tax reforms.

Overall, I think the best approach when introducing proposals of this type is to show how they can raise the same amount of revenue as the current system under current economic conditions and then to argue that there will also be a positive but uncertain boost from supply-side effects.

Impact on Inequality

To understand the impact of flat tax proposals, it is necessary to have a fully-worked example that shows how households in every part of the income distribution will be affected and how the taxes raised add up to match the revenue of the existing system. As far as I know, RENUA have not provided these calculations but I have put together a spreadsheet using data from the Revenue Commissioners to illustrate two different types of flat tax system. My conclusion is that any system that features a 23 percent tax rate and raises the same revenue as the current income tax and USC combined will be sharply regressive in its impact on income distribution.

To do these calculations, I used income distribution statistics from the Revenue Commissioners. The figures show numbers of tax payers in various income bands, the total amount of income they earned and the amount of tax they paid. Specifically, I use the table that shows the combined amounts of income tax and USC paid by various groups.These are in the tab labelled “Basic Data”. The figures I use are from 2011 and are from the 2012 “Statistical Report”, a publication that the Revenue appear to have discontinued. While it would be nice to have more recent data, the figures are sufficient to model the effect of tax reforms in a realistic manner.

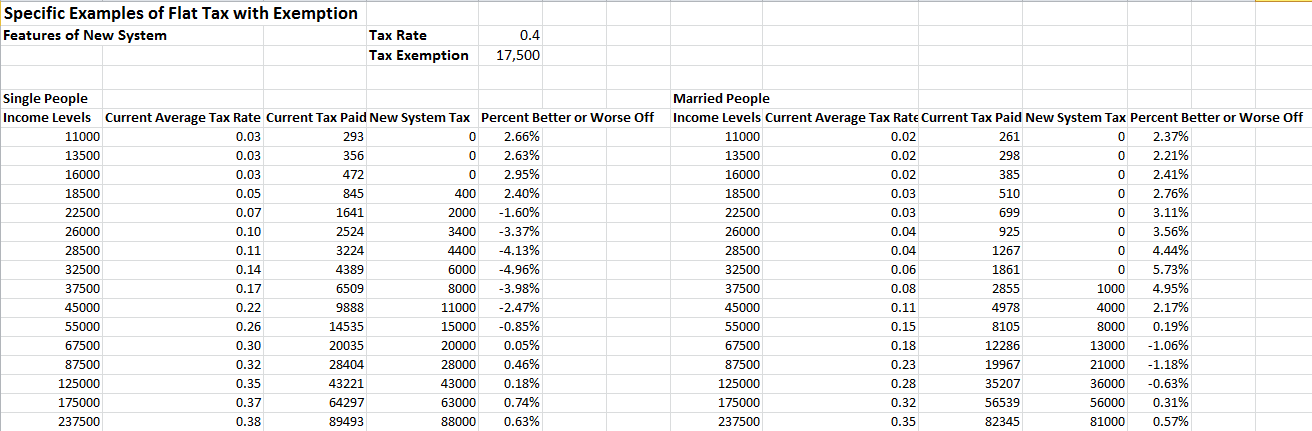

See below for a summary of the tax paid by various groups in 2011. I have aggregated data on single-earner and double-earner married people as well as various classes of single people to keep the figures as simple as possible.

A couple of aspects of these calculations are worth emphasising. First, Ireland’s income tax system is extremely progressive with very low average tax rates for people at the lower end of the income distribution. Single people earning under €20,000 and married couples earning under €30,000 both are taxed at a rate less than 5 percent.

Second, the figures show that the richest are shielding large amounts of money from income taxation. For example, the richest group of married people (those earning over 275,000) earn an average of just over €500,000 per year but pay an average income tax rate of only 39 percent. Given how much of their income is supposed to be taxed at a marginal tax rate of about 50 percent, this suggests a significant amount of shielding of otherwise taxable income.

The spreadsheet describes two different variants on the flat tax. The first variant has a single tax rate as well as tax-free exemption on the first portion of income earned. The second variant has a single tax rate and a specified tax credit that is available to all. I have assumed that married couples get a double tax exemption or double tax credit depending on which system is examined. The spreadsheet allows the user to enter their chosen tax rate as well as their preferred tax exemption or tax credit. It then shows the resultant tax rates for various groups and compares them with the current system (or more precisely the 2011 system, which was very similar). Finally, it calculates the total amount of tax revenue raised by the current and reformed systems.

For both the tax exemption and tax credit system, I have entered 23 percent as the flat tax rate and then adjusted the other aspect of the tax system so that the total amount of money raised more or less matches the current system. For the tax exemption system, the size of the tax exemption that allows the reformed system to raise the approximately same amount of revenue was €5,000. The table below shows the details. It is very small but (at least on my computer) clicking on it makes it bigger. The tax rates for those at the bottom end (apart from those earning under €10,000) would be significantly higher and tax rates for those at the high end would be significantly lower.

This table (from the the tab “Specific Examples”) reports the scale of income losses and gains to various groups.

The proportional gains at the top and losses at the bottom are very large. A move to a tax system of this sort would greatly raise post-tax income inequality.

Of course, the RENUA proposal is a bit more like the “tax credit” variant due to the guaranteed income of €8,000. In my calculation, the tax credit that allows a 23 percent rate to raise the same amount of revenue as the current system is only €1,140. It is possible, however, that this is somewhat consistent with RENUA’s plan because most of the money for their proposed guaranteed income would presumably come from the existing social welfare system. In any case, the tax rates from this tax credit system are basically the same as those from the exemption system.

A Fairer Flat Tax?

This doesn’t mean that flat taxes have to be innately unfair. For example, you can use the spreadsheet to show that a flat rate of 40% with a tax exempt allowance of €17,500 would raise as much as the current system and still be highly progressive. However, there will always be winners and losers from tax reform. A system of this sort would see married people with joint incomes under €50,000 register gains but they would take these gains from single people earning between €25,000 and €40,000.

So no tax system is perfect or will be favoured by everyone. What this example does show, however, is that it is possible to have flat tax rate that is a lot lower than the current top marginal rate without having a significant increase in inequality. A system of this sort would likely have some positive effects in reducing tax evasion and could have some of the positive supply-side effects described by RENUA. However, the idea that we can have a headline tax rate of 23% without greatly raising inequality does not hold water.

So no tax system is perfect or will be favoured by everyone. What this example does show, however, is that it is possible to have flat tax rate that is a lot lower than the current top marginal rate without having a significant increase in inequality. A system of this sort would likely have some positive effects in reducing tax evasion and could have some of the positive supply-side effects described by RENUA. However, the idea that we can have a headline tax rate of 23% without greatly raising inequality does not hold water.

Presentation on the Irish Economy

I gave a presentation today on the outlook for the Irish economy at the annual conference of the Regional Science Association International (British and Irish Section). The presentation was considerably more upbeat than many I have done in recent years but still discusses a number of important medium-term risks to the economy. Slides are here in PowerPoint form and here in PDF.

The Central Bank and the Irish Property Market

Last week, the Central Bank of Ireland published an important consultation paper. Despite the boring title (“Macro-prudential policy for residential mortgage lending”) this is a very important initiative that will have profound implications for banking and the Irish property market.

The paper proposes the introduction of restrictions on Loan-to-Income (LTI) and Loan-to-Value (LTV) ratios for Irish residential mortgages. Specifically, it proposes that a maximum of 20 percent of loans should have LTIs over 3.5 and that a maximum of 15 percent of loans should have LTVs in excess of 80 percent. The latter, in particular, would represent a significant departure from the lending standards seen in Ireland over the past few decades.

Given the recent experience in Ireland and elsewhere with property bubbles, I agree that measures of this type need to considered as part of the regulatory policy kit. So, as a general matter, the Central Bank are to be congratulated for being willing to introduce this type of regulation despite its inevitable unpopularity in certain quarters.

In particular, I support the proposed LTI restrictions. These restrictions may be unpopular now with first-time buyers. For example, someone with an income of €50,000 will now be told that the most they can borrow is €175,000. This may appear to reduce their ability to purchase a house if, for example, they had previously planned to borrow €250,000. However, evidence from previous cycles has shown that more generous mortgage credit tends to drive up house prices. This has meant that first-time-buyers end up chasing their own tails, as they all take on additional debt without actually being able to buy better houses. I would be confident that, over time, the LTI limits will restrain house prices and allow first-time buyers to obtain a home without being burdened with huge debts.

That said, I still have some concerns about the way these measures are being introduced and about their timing. In particular, I have reservations about the rapid introduction of an 80 percent LTV standard.

Consultation and Debate

After the global financial crisis, it has become widely accepted that macroeconomic policy-makers need to look beyond using only short-term interest rates to control the economy. Restrictions on LTV and LTI ratios are examples of a set of policy options that have become known as “macro-prudential policy” i.e. policies that are aimed at protecting the stability of the financial system as a whole rather than just focusing on each financial institution separately.

Central Banks, as financial regulators, will generally be the organisations imposing macro-prudential policies. This has caused some debate about the implications of independent central banks setting a much wider range of policies than in the past. Here, for example, are some thoughts from the IMF’s chief economist, Olivier Blanchard.

If you think now of central banks as having a much larger set of responsibilities and a much larger set of tools, then the issue of central bank independence becomes much more difficult. Do you actually want to give the central bank the independence to choose loan-to-value ratios without any supervision from the political process. Isn’t this going to lead to a democratic deficit in a way in which the central bank becomes too powerful? I’m sure there are ways out. Perhaps there could be independence with respect to some dimensions of monetary policy – the traditional ones — and some supervision for the rest or some interaction with a political process.

I don’t claim to have all the answers as to how these new tools should interact with the political process. Still, I do think the Central Bank’s approach appears to be at odds with Blanchard’s ideas. The approach being taken to debate and consultation has been pretty minimalist.

These policies will have a direct effect on the housing decisions of many people and will probably also have important indirect effects. As such, I believe the measures should have been subjected to a longer and more rigorous consultation process, involving a series of public meetings and Oireachtas committees prior to the specific proposals being tabled. As it is, the Bank is announcing a very short consultation process with the plan being to take comments up to December 8 and then introduce very substantial changes to mortgage lending in January.

Cyclical Considerations

One of the themes of academic work on macro-prudential policies is that these policies should be used in a cyclical fashion, tightening credit during upturns and allowing it to be loosened during downturns. My reading of the recent international evidence on the use of LTV caps is that they are being used in countries where the authorities are very concerned about the risk of a housing crash, with the implicit policy being to ease these restrictions when this risk is lower.

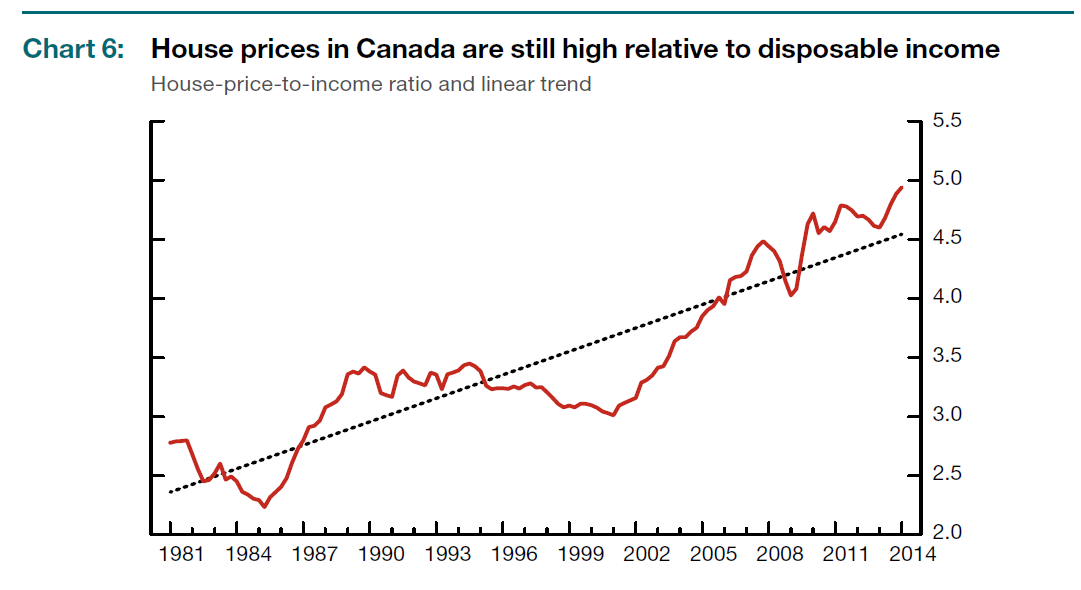

For example, Canada is a widely-cited example of a country where a set of restrictions on LTVs have been introduced, with maximum LTVs gradually being reduced from 100 percent in 2008 to 80 percent in 2012 (along with various other measures – see this summary from the IMF). However, it is worth emphasising that these measures have been put in place because the Canadian authorities view a large housing crash as a significant possibility. Here is a chart from the latest Bank of Canada Financial System Review showing a steady rise in housing valuations.

The commentary in the report views a housing crash as a potentially severe threat to Canadian banks and the restrictions on lending are being put in place for this reason.

New Zealand is another example of a country that has introduced LTV restrictions, with loans with LTVs above 80 percent now restricted to be no more than 10 percent of the total amount of mortgage lending. Here is a nice paper from the Reserve Bank of New Zealand describing the restrictions. An important message from this paper, however, is that the RBNZ views these restrictions as an explicitly temporary policy.

LVR restrictions are to be used only occasionally, at those points in the financial cycle where there is a real danger of growing systemic risks leading to financial instability. The Reserve Bank does not intend to operate LVR restrictions in a continuous fashion to smooth the cycle, but rather aims to limit the extreme peaks in house price and housing credit cycles.

This raises questions about the current situation in the Irish housing market. Is Ireland now in a situation where, in the absence of these policies, there would be a significant risk of a crash over the next few years?

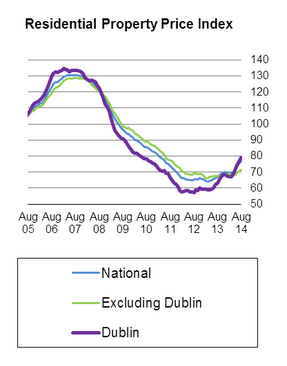

Residential property prices are certainly growing a very fast pace, up 15 percent in the year ending in August. But, as the picture below shows, prices are still very far off peak levels.

More broadly, valuations look to be in line with the more sustainable levels seen prior to the housing boom. For example, the ratio of prices to rents is back at levels last seen in the late 1990s.

The Central Bank’s new policies are focused on restricting the downside of house price declines by restricting the provision of mortgage credit. However, the current trend of rising prices is not in any way related to easy mortgage lending. Indeed, the Central Bank’s own statistics show that the total stock of mortgage credit continues to decline at about the same pace as it has over the past three years (see the red line below).

Rather than being driven by credit, the evidence points to a shortage of supply as the main factor driving house prices. After the building binge of the Celtic Tiger years, housing completions have slumped. Indeed, given trends in population and household formation, we now appear to be at the point where the previous period of over-building has now been offset by the cumulative under-building of recent years.

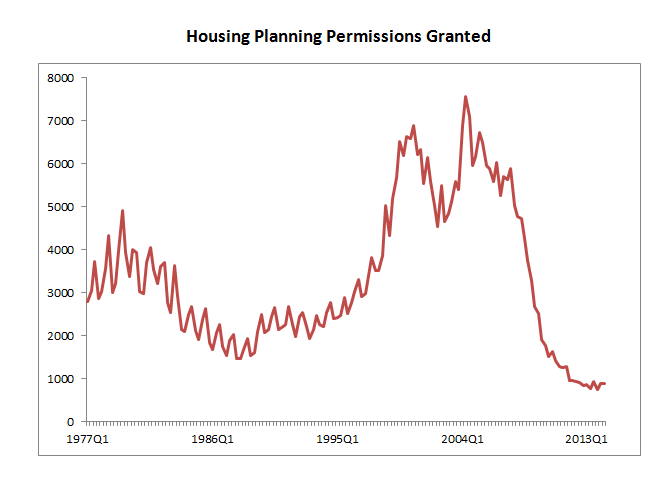

Nor does it appear that recent price increases are doing much yet to provoke a supply response. Planning permissions remain at historically low levels. Anecdotal evidence suggests restrictions on the supply of credit to builders as well as a raft of cost-increasing building regulations are at least partly responsible for this lack of supply response.

Against this background, there are reasons to be concerned about the potential impact on the housing sector of the proposed 80 percent LTV requirement in January. As of now, most first-time buyers have been focused on saving about 10 percent of the value of the home. Particularly for those who are also currently paying rent, coming up with this 10 percent is already a challenge. An instant doubling of this requirement would likely force a large number of potential purchasers out of the market, as they would need to wait another few years to double their savings.

This measure may well end up stabilising house prices but it may reflect the deliberate engineering of a nasty equilibrium, one in which Central Bank regulations lead to low demand for new house purchases, matched on the other side by a low level of supply due to credit and other regulatory restrictions. Meanwhile many potential buyers (particularly those unable to sufficiently tap the Bank of Mum and Dad) will feel squeezed out of home ownership and forced to rely on Ireland’s chaotic rental market or its already-inadequate supply of social housing.

At this point, my assessment is that conditions in the Irish housing market do not currently point towards the need for a sudden large change in LTV limits. Whether a gradual introduction of higher LTVs is desirable is a more open question.

LTV versus LTI Restrictions

I noted above that the situations in which countries like Canada and New Zealand have introduced LTV restrictions look quite different from the situation in Ireland today. Indeed, it seems highly unlikely that the authorities in Canada or New Zealand would be imposing 80 percent LTV caps if their property market looked like the current Irish market.

In addition, it is worth noting that LTV restrictions are not a necessary part of the macro-prudential toolkit. The UK has also begun adopting macro-prudential policies aimed at cooling a property market that (in places anyway) shows signs of being genuinely over-heated. However, the Bank of England’s new guidelines have focused solely on LTI restrictions rather than limits on LTVs.

Even in expansions, LTV limits can have unfortunate knock-on effects. Here’s a nice article from the Telegraph on macro-prudential policies. It contains the following observations from Adair Turner.

“The trouble with LTV is it can be a bit circular. You impose an LTV limit and the price can go up, and then somebody can borrow more money via a mortgage on the price that’s gone up,” he says. “One of the problems we have in our economy is the way in which we borrow money against the value of an asset which goes up, which appears to make more borrowing justified. LTI targets the real thing, which is: can people repay the debt out of their income?”

In this sense, a policy framework that focuses too much on LTV restrictions can enhance the fundamental pro-cyclicality that is already in place with existing banking regulations.

Needed: An Integrated Housing Policy

The benefits to financial stability of requiring a large deposit before purchasing a house are clear. Banks are less likely to lose money on home loans in a downturn once the owners have put in more equity. However, the risk associated with falling house prices in Ireland are relatively low at this point and the sudden imposition of an 80 percent LTV norm will have implications for society that go well beyond banks.

It’s not rocket-science to point out that anything that makes it harder for people to purchase something (an inward shift in the demand curve in economist jargon) will result in a lower amount of purchases of that item. The imposition of significantly higher LTVs will likely delay the age at which younger people can purchase homes and will increase the amount of people who will never be in a position to purchase a home.

But housing is special in the sense that we all need a roof over our head, so any policy that reduces people’s ability to purchase homes needs to be matched with a policy that helps them with alternatives such as social housing or long-term renting. Ireland is currently doing a horrible job in this area. The boom provided an opportunity to build up a good stock of high quality social housing but governments decided they had other priorities. Renters also have relatively weak rights, meaning those who want long-term security feel they must own their own home.

These are all issues that the government can act on over the next few years. So I have no problem with Ireland setting a long-term target of an 80 percent LTV norm in the context of a sensible integrated housing policy. But I believe the conditions for the macro-prudential use of LTV restrictions do not apply to the current Irish housing market and that LTI restrictions make better macro-prudential policy tools anyway. As such, I fear the unintended consequences of the LTV policy may outweigh its perceived longer-term benefits.

The concluding lines of the Reserve Bank of New Zealand paper by Lamorna Rogers (cited above) are relevant to the current debate in Ireland.

LVR restrictions provide a way of restraining housing demand while working on the supply response. But in the medium to longer term, imbalances will need to be resolved through appropriate longer run policy measures, including actions to improve the housing supply.

It is, of course, crucially important that Ireland does not return to the irresponsible mortgage lending of the last decade. However, what is required now is more than that: Ireland needs a coherent joined-up housing policy. Ideally, it would be better to debate restrictions on LTVs as part of this broader discussion instead of imposing them for financial stability reasons irrespective of the other parts of the policy framework.

Cantillon on Central Bank Bond Sales

I seem to have annoyed someone with my post about the Central Bank’s bond sales, judging by this discussion of the issue by the Irish Times Cantillon column.

When the promissory notes were swapped for long-term bonds held by the Central Bank last year, various people pointed out that the faster the pace of sales of the bonds to the private sector, the smaller the gains from the swap would be. See for example, my post on this and also Seamus Coffey’s similar conclusions. I don’t recall anyone disputing this point at the time.

Now, however, Cantillon is here to tell us that this point is “simplistic”. Apparently, it “ignores the fact that the bank cannot hold the bonds to maturity.” So who is doing this ignoring? Not Seamus. Not me – our calculations on this have always assumed the Central Bank will sell the bonds.

What then about all this stuff about this being a great time to sell the bonds? You wouldn’t know it from Cantillon’s long-winded discussion but this really is a pretty simple issue. If we sell the bonds now, we start paying interest straight away and this adds to the cost for the Exchequer.

Of course, it is possible that yields on Irish sovereign bonds may rise so much in the future that we could end up paying more in interest by delaying the bond sales—we extend the period of time that cost is zero but at the expense of much higher interest costs later and this latter factor ends up dominating. With the ECB committed to low interest rates for the foreseeable future, the Irish economy recovering and the debt-GDP ratio falling, this doesn’t seem like a scenario we need to worry too much about.

Cantillon’s final point – that ultimately what’s going in is that faster sales “diffuses at least some of the anger felt in Frankfurt that Ireland in effect obtained monetary financing for itself via the deal” – is of course spot on. Alas, little is likely to be done to diffuse the anger felt in Ireland about the ECB’s actions during the crisis.

In Ireland, Even Bad News is Good News: Bond Sale Edition

There is lots of good economic news coming out of Ireland these days. GDP is rising at an impressive rate, unemployment is falling, government bond yields are very low and the public finances are improving significantly. In fact, things are so great now that even unmitigatedly bad news is presented as good news.

Thanks to Lorcan Roche Kelly for alerting me to this gem this morning.

.@LorcanRK Wow, a truly impressive amount of wrongness stuffed into one little article. The IT has really set new standards with this one.

— Karl Whelan (@WhelanKarl) September 26, 2014

So why is the Irish Times article so bad? It reports that the Central Bank is speeding up its sales to the private sector of the bonds it received in place of the promissory notes and that it is now going to sell more than the minimum pace of sales signalled last year. The article clearly signals to readers that this is a piece of good news and does not suggest any downside. The reality is that there is no upside whatsoever to the sales. This is a bad news story all the way.

Why is this? The current arrangement features the Central Bank owning bonds issued by the government. The government pays interest on these bonds, these interest payments add to the Central Bank’s profits, and then these profits are eventually recycled back to the government. So as long as the Central Bank holds on the bonds, the net cost of this debt to Exchequer is precisely zero.

What happens when the bonds are sold to the private sector? The annual interest payments now go to private sector investors and don’t get recycled back to the government. So the cost is no longer zero.

The replacement of the despised promissory notes in February 2013 with the new bonds acquired by the Central Bank was widely presented as a big improvement for the Irish state. However, economists emphasised at the time that any benefits depended on the pace of sales. See, for instance, the bottom part of this blog post, which illustrates how a faster pace of bond sales can undo most of the perceived benefits of swapping the promissory notes for longer-term bonds.

But surely there must be some goods news here? What of these capital gains the article refers to? This has occurred because Irish government bond yields have fallen since these bonds were issued to the Central Bank. This means they can be sold for lower yields than the par value they had when the Central Bank purchased them, thus implying a profit on disposal.

The private sector investors who buy these bonds will receive the coupon payments set out in the original bond contracts (they pay Euribor plus 263 basis points) but the capital gain made by the Central Bank means that, on net, the interest cost of the sold bonds to the Irish state will equal the new lower yields. Again, the idea that movements in bond yields would influence the ultimate cost of these bonds was flagged in various discussions of the operation last year, include my own post on it.

So the good news here is the Irish government bond yields have fallen and the net cost of selling these bonds is lower than it would have been a few months ago. But selling them at all still means the cost of these bonds goes from zero to positive: From now on, the bonds are going to have an annual cost to the Exchequer, whereas as long as the Central Bank held them there was no net cost at all. A faster pace of sales thus raises costs for the Exchequer.

Like I said, not a good news story.

Monetary Financed-Related Addendum: One point I omitted when I posted this is the following. Some may read this and say: Why can’t the Central Bank just hand back all of the money it receives from the bond sales to the government, not just the capital gain? The answer is that this would violate the agreement the Central Bank has with the ECB via how to unwind the Anglo situation.

The Central Bank loaned over €40 billion to Anglo\IBRC, most of it in the form of Emergency Liquidity Assistance. This involves the creation of new money. The ECB wanted to see the money issued in this fashion retired from circulation when the loans are repaid. IBRC was liquidated without repaying the loans and selling off the new bonds is the current method the Central Bank has agreed with ECB for how this money is to be retired (or “extinguished” as Patrick Honohan puts it).

So if the Central Bank received a bond with a face value of €1 billion, then a sale of that bond to the private sector should result in €1 billion in money being retired. I’m guessing, however, that if the bond is sold for €1.2 billion because yields have fallen, then the Central Bank gets to keep the additional €0.2 billion and still only retires €1 billion.

Alternatively, all of the €1.2 billion goes towards “extinguishment” but this process could mean we still have some bonds left over (which could be retired from the national debt) once the extinguishing is over. Either way, the €200 million capital gain in this hypothetical example reduces the ultimate net cost of the bond sales but does not change the fact that faster sales are bad news.